Talent, Value Distribution, & Liquidity in Crypto Protocols

Thinking through some of the dynamics of how liquidity, vesting, and lockup perceptions have changed and how much optimization is left to be done on structuring this within crypto.

To read the full version of this post with footnotes click here

There has long been discussion and divisiveness on startup equity in crypto. Most recently signified by Mike Dudas’ tweet above surrounding how crypto fixes the illiquidity and binary nature (at times) of startup equity.

I made the point that there is an illiquidity premium that arises in startups that allows a power law driven nature of returns, and keeps people from dumping their equity during valleys of despair.

Crypto theoretically wouldn’t save you from that. And as we’ve seen historically in crypto, the dominant move has been to largely never sell.

But as industries mature, dynamics continue to change, and crypto is speedrunning these primitive evolutions both on the capital markets side, compensation side, as well as the industry competitive dynamics side of things.

In 2017 during the ICO run, many of those teams barely had any lockups or vesting. They promised decentralization with a foundation that would then allow some oversight, but in reality, many projects were money grabs that resulted in capital raises that allowed insiders to dump tokens nearly immediately.

Any person who had been in startups before could have told you that was poorly aligning incentives. Of course, as there is an imbalance of supply and demand, the supply side can bend norms in order to fulfill demand. We see this now in tech with flexibility of work arrangements, in investing with looser board governance, and in capital market relationships with LPs allowing VCs far more latitude than perhaps ever before.

During the 2017/18 market, many investment firms weren’t happy about being locked up for material timeframes in a soon-to-be liquid asset. This allowed firms like ours (Compound) to take multi-year lockups happily and (barely) differentiate on the axis of patient capital. This was appreciated by founders at the time, but partially the most honest answer was that we didn’t view our expertise in short-term value creation at the time and again, viewed the illiquidity as a premium.

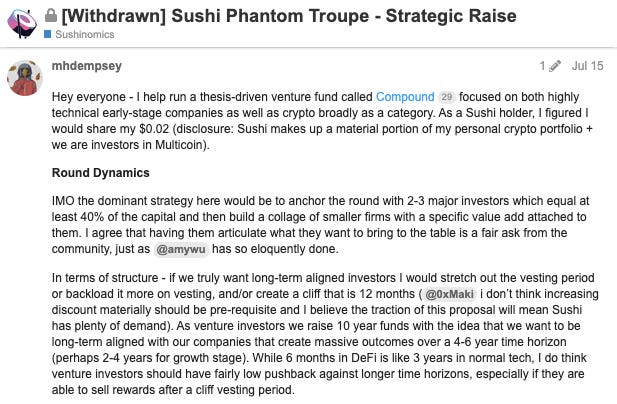

With the Sushi Phantom Troupe strategic raise we saw the overton window of lockups and discounts shift, as VCs negotiated against themselves (myself included) to have further dated lockups and eventually to even pay a pre-negotiated premium to the public token price using various instruments (most notably the UMA Success token).

There are perhaps two polarizing ways to look at this:

Web2 players understand how to optimize for asymmetric, long-term value creation better than any other collection of people in an industry. The learnings from decades of turns at this have created an optimized machine, as long as the industry is willing to accept power law outcomes and a high failure rate. This last part is largely because of the lack of churn that exists within the industry, meaning that you if you stay in “web2/tech” for long enough, you drastically increase your chances of improving your filter and finding a piece of a power law outcome.

Crypto is the natural evolution of power law distributions pushing a bit less concentrated with ability to vest into liquid assets quickly, where those assets are priced at some form of terminal value by a larger collection of buyers (versus private markets where price is set by a small # of buyers), and often are supported by this large collection for years even if the projects are effectively zombies. These dynamics thus should be viewed as the next learning (for Web2 and Crypto) as worker dynamics have changed (multi-project, shorter-term tenure) as well as pace of innovation has increased (a year in crypto is 3 years in tech).

The reality is of course, in my opinion, somewhere in the middle.

On Web2 – Employee value capture is still misaligned despite the imbalance of supply and demand of talent. I’ve argued that Web2 companies much shift their vesting schedules in a way to adapt to the market as well as make the expected value of being a startup employee as attractive as joining growth stage startups, big tech, or perhaps Web3 projects. This will manifest itself in shorter vesting schedules (into a still illiquid asset) as well perhaps larger option pool allocations.

On Crypto – Core contributors, engineers, and other full-time workers will have power for some time. However, as more talent enters the space the supply-demand imbalance will fall and with the maturation of crypto, two things will happen.

First — we will see a higher % of projects fail. This is natural. There will be more projects started, capital markets will support them with a near insatiable appetite, and at any downward turn in the market, a percentage of tourists will leave for safer/more familiar pastures. Crypto broadly has likely not reached the perpetual negative churn rate that Web2 did for the prior two decades, thus you will have some percentage of people who get burned and take another bull cycle or two to return to Crypto. The failure will come from the market side, execution side, as well as the talent side.

More advanced vesting schedules and lockups will curb the ability for contributors to dump their tokens quickly before that failure point, creating a similar dynamic perhaps as Dudas discusses in his original tweet, of people sitting on largely illiquid massively devalued tokens.

Second – I have been very vocal that crypto projects will begin to notice the value accrual and strategic importance of building more platform centric or horizontal protocols, leading to an expansion of their scope of ambition. This could lead to a dynamic where the talent market begins to actually look more like early Web2 than it does today, a time where talent flowed less freely between startups and eventually as the industry solidified, focused on compounding value of their existing holdings over multiple years or a decade.

This could be enabled by the first $100B+ (or $1T+) application layer protocol, which will open the eyes to contributors about the potential for value capture by working long-term on building a suite of products that compete against singular focused projects. We see this with unbundling and rebundling in Web2, and it’s likely Web3 will experience similar dynamics (hopefully this doesn’t look like the same team launching a bunch of tokens for each project).

This could also come from projects controlling their liquidity more, perhaps zagging from the market and not publicly launching their token until later into the development cycle, or a variety of other mechanisms which will allow for value accrual to sit with the builders and partially whitelisted financiers versus the entire market of builders, speculators, and financiers.5

All of these dynamics are still to be sorted out but my broader point is that we have not nearly optimized or innovated on the structuring of distribution of value/wealth to builders within Crypto. While the liquid nature of crypto is what brings many to the table, we shouldn’t disregard the potential leverage that forms of illiquidity could create. Nor should we assume that what holds today as valuable to the builders is what will hold tomorrow. In wars for talent, capturing and retaining the talent can be fickle, and as humans flow into the industry, it’s important to be on the frontier of understanding these dynamics and how new entrants may not pattern match precisely to prior incumbents.