On My Mind # 5

Small dataset ML, All VCs short startups, We're in a restaurant bubble,

5 things on my mind - by Michael Dempsey

What an intermission. We’re back. Hopefully every 2 weeks. This email spawns from this thread. The process for this will continually evolve but as you'll see, some thoughts are random, and most are unfiltered or poorly edited. Either way, let me know what you like, don't like, or want to talk about more.

5 Thoughts

1) The over-intellectualization of thought. A tweetstorm.

“Someone had to say it”. Here.

2) We may be in a restaurant group bubble because unlike technology, restaurants aren’t nearly as scalable or profitable.

A decade ago there were a significantly smaller number of restaurant groups with multi-geo expansion goals. Similar to startups, in restaurants we now have poster-children and idols for new restauranteurs with large ambition, we have lots of capital that has flooded into private markets to fund this expansion, and we have clear trends that people can coalesce around (analogous to enabling technologies).

Zuckerberg (web 2.0) could be viewed as Danny Meyer who made tons off of successfully scaling Shake Shack (early displacement of fast food), and some off of USHG (dirty secret here, Shake Shack yelp reviews outside of NYC are significantly worse than in its hometown). Related read on USHG here.

Evan Spiegel (mobile) could be viewed as the Sweetgreen team, who scaled the next main platform, QSR, via trends of healthy, premium, narrative-driven food in a post-McDonald’s/Chipotle world.

David Chang of Momofuku fame fits somewhere between the two generations. He was responsible for pushing a certain aesthetic and lust of international, full-service cuisine in the US, while also being tempted into other paths that failed (Lucky Peach, Ando, Maple). Maybe in an unfair world, he’s Ev Williams (Twitter -> Medium)? The difference being now Chang is on a capitalistic hellbent path for Fuku (his fried chicken sandwich concept) expansion.

These idols, capital sources, and strong trends now have created a moderate bi-furcation of restauranteurs. Either you are a sole proprietor with maybe a sister location within your city or you’re someone who was this, but now with a solid Michelin mention, NYTimes, Infatuation, or Eater review you’re scaling to 2-5 more restaurants and thinking about how quickly you can move to LA, SF, NYC, Miami, or (god forbid) Las Vegas.

Modern Restauranteurs have looked at this niche consumer trend, and general rejection of chains, with a view that their concept scales. The issue is, many don’t. They don’t because of supply chain/economics, they don’t because of operational consistency, and they don’t because in each city they are moving into, there’s someone just like them (or is about to be) to compete with.

Restaurants don’t feel like they should be a power law industry, but I don’t think returns will be as evenly distributed as many fast-expanding restauranteurs believe. There is a glut of restaurants that work in core markets at high prices and continue to try to expand rapidly on full service without understanding the complexity. And this will lead to a graveyard of formerly great restaurants that will scale back if they’re lucky, or die.

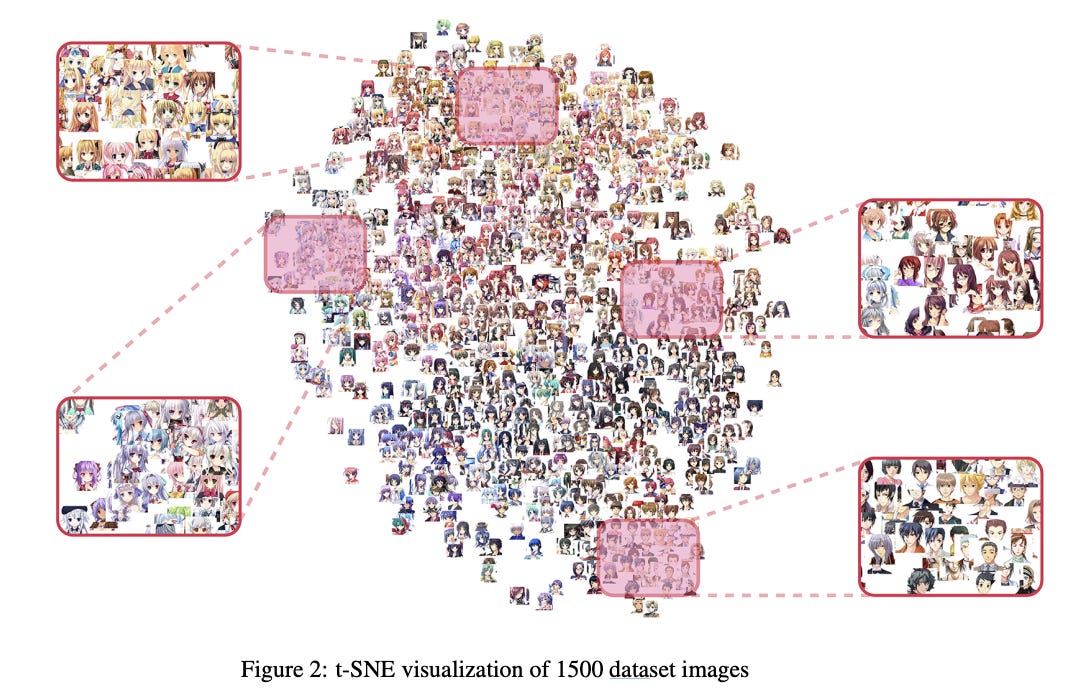

3) Small dataset machine learning is more important than you know.

One of the big areas of machine learning I've been focusing on has been small dataset tools. The dirty secret within many creative ML models is that the scale and cleanliness of the data is remarkably high. For example, one of the earliest papers on generating anime faces features a dataset with close to 50k images all with varying (but closely cropped) head poses. More recently, Nvidia’s StyleGAN paper used a new dataset of 70k images (FFHQ) in order to have more variation, leading to better diversity and quality of generation. What we've started to see now is people experiment with new forms of transfer learning to transfer a pre-trained model onto a new domain. This paper showed this with just 25 new images onto a previously trained model at one point. I expect to see this trend only increase as few practitioners have the budgets or time to properly curate a dataset. In addition, many emerging use-cases may traditionally need a dataset size which is impossible to gather.

4) Remember shorting is capped upside, unlimited downside. Also, all VCs sorta short startups implicitly.

Friends know I am fairly active in shorting stocks in my personal public market portfolio and often enjoy talking about that more than longs. Being able to identify faults in public companies, when most external pressure has pushed them to continue to rise in value over the past decade is a valuable skillset and fascinating though process. I think the stance that some in VC take that we are long-only investors is an overly literal one and is either a mis-evaluation of what exactly our job is, or is a marketing ploy.

As venture dollars have flowed, and very few startups are *truly* one-of-a-kind from a business model perspective, venture investors are forced to place bets on outperformance and underperformance across categories, and because we largely operate with the belief that we are investing in duopolistic markets, our companies are often near zero-sum. Thus, while we are only allocating dollars to long positions, we implicitly are making decisions based on being short other businesses.

With respect to public market shorts, the one thing to realize when taking a financial position is that upside is capped in shorts (a stock can only fall 100%, but can grow infinitely). What this means is 2 things.

First, most people shouldn’t short stocks. Markets trend up over time and there’s tons of literature as to why holding and participating in key rally days drastically impacts returns.

Second, sometimes it's dominant in the short to mid-term to take a market neutral stance (a less-correlation reliant version of a pairs trade) so that you are only making an implicit competitive bet. An example of this in practice would be going long Uber and short Lyft at the same time and constantly re-balancing these positions as they develop so that your financial success is merely tied to Uber outperforming Lyft, not Uber ultimately winning.

5) Construction sites feel like the next battlefield for robotics after factory floors.

There are so many startups in this space.

If you have any thoughts or feedback feel free to DM me on twitter. All of my other writing can be found here.